Vistry Group PLC

1. Thesis:

Vistry, a UK home builder, is shifting from a conventional buy land, build-and-sell approach to a leaner partnerships model. By collaborating with housing associations and institutional investors, Vistry avoids expensive land purchases, focusing instead on constructing pre-sold, affordable homes.

This approach is more capital-efficient, shortening cash conversion cycles compared to traditional homebuilders. With up to half of its homes pre-sold, Vistry ensures quicker capital turnover. As this transformation advances, the company anticipates a return on invested capital exceeding 40%, surpassing the 15% typical of conventional builders.

The UK’s housing shortage exceeds four million homes, with affordable housing shortages being the most acute. Vistry is well-equipped to address this need, leveraging their extensive network of over 60 local authorities and their modular construction expertise (via Vistry Works). Additionally, its contracts lock in margins, ensuring the company meets its ROIC goals.

By redirecting resources from its traditional operations to partnerships, Vistry expects to unlock over £1 billion for shareholder returns through buybacks—a significant amount given its £2 billion market cap.

VTY has set their medium-to-long term targets as follows:

1. ROCE of 40%

2. Ebit of £800m

3. Ebit margin of 12%

2. Discussion

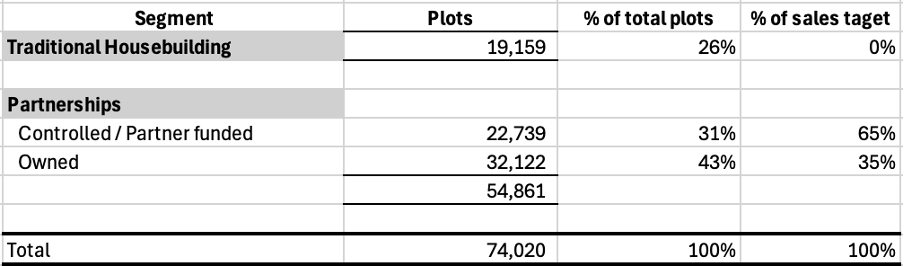

The above is essentially the thesis management is selling to investors. This sounds extremely attractive; however, I have questions. Primarily it is not clear to me how exactly they intend to unlock £1bn to deploy to share buybacks. Below is their current landbank/plots.

VTY is running off their traditional housebuilding business. They are not replacing these plots as they sell them off. What is not clear to me is whether they are just going to (1) sell these plots to another housebuilder(s) or (2) if they are going to complete building houses on them and then sell the plots+houses to customers. Option 1 would be quicker and would raise about £800mn (each plot is held on their books at about £40k).

The problem is that they have also stated in their annual report that they aim to have a 4yr landbank. Considering they currently sell >17k houses per year, it implies they need a 68k landbank. This would be split between controlled and owned plots. Their aimed split between the two is 33% controlled and 67% owned. Thus:

Controlled = 68k * 33% = 22K plots (Currently they already have 22.7k controlled plots)

Owned = 68K * 67% = 46k plots. (Currently they only have 32k owned plots)

This means they would need to purchase an additional 14k plots to bring their owned plots to their desired level.

So, they might sell the 19k plots in their traditional homebuilding segment, but they would also need to purchase 14k plots in their partnership business. Essentially on a net basis they would only be selling 5k plots – raising £200m.

With option 2 – completing construction on the plots and selling the plot+house, they would likely earn around £1.1b. This is because they earn about £20k ebit per house, but you need to add the value of the plot being sold (£40k) as well since they aren’t replacing these plots. This equates £60k ebit per plot+house and they have 19k plots in their traditional homebuilding business which adds up to £1.1b. You then need to subtract the ~£560m they need to spend to bring the owned plots in their partnership business up to their desired number. This would leave them with £540m to return shareholders. This is better than the £200m they would have available for buybacks under option 1.

The above is why I think it is unlikely they actually manage to buyback £1b of shares as they run-off the traditional homebuilding business. However, a £540m buyback is still nothing to scoff at, considering it equates to 25% of their current market cap.

Another curious disclosure is VTY’s target breakdown of their landbank, between controlled and owned land, and their % sales breakdown of those plots. From the annual report:

· Over the medium term, we expect around one-third of the land bank to come from controlled (partner funded) rather than owned sites, as controlled sites require only minimal upfront capital investment.

· On average we are targeting c. 65% of the units to be Partner Funded sales.

The above targets can be summed up in the below table.

From the above, it is strange to me that they aim to own 67% of their land bank while sales of owned plots make up only 35% of sales. Naturally the less land they own, the higher their ROCE will be, so the target structure seems sub-optimal. Maybe there is a rational reason for this structure, but I don’t have the answer. Were the land bank % breakdown to match the sales %, I would have no reservations/doubts about the proposed £1b share buybacks.

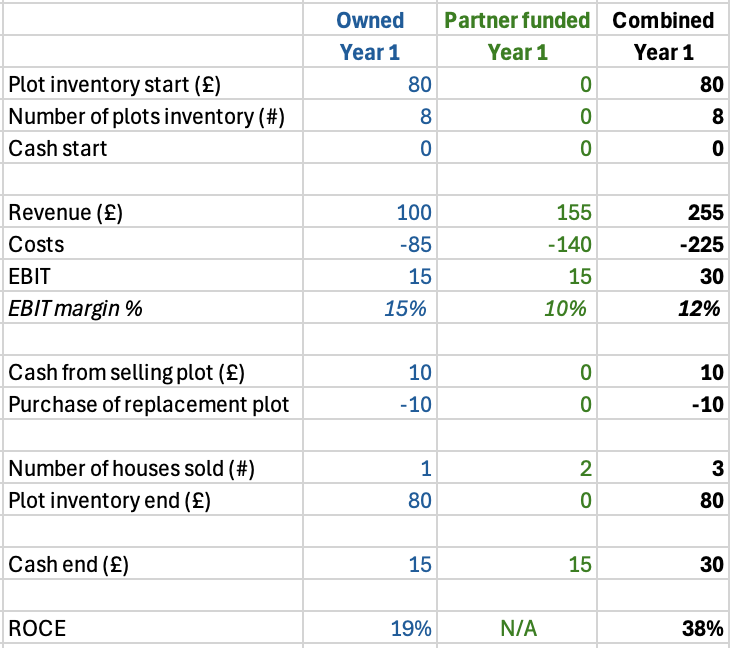

3. Theoretical model

To simplify the proposed partnership model and see if the >40% ROCE is realistic, I simplified it in the following way:

Assume they sell 3 houses a year. 1 house sold in the owned segment and 2 houses sold under partnerships. This closely follows their aimed split of 35%/65% between owned and controlled.

They have 8 plots on their balance sheet. If they sell 3 houses/plots per year and have a 4yr landbank that equates 12 plots, but they only own 67% of these = 8 plots.

Standardised revenue per house to £100 and indexed all other costs to that £100 according to the actual expenses as a % of revenue.

*The cost per plot is calculated as follows: £40k per plot divided by avg open market sales price of £385k = plot is 10.4% of sales price. i.e. an empty plot costs £10 in the above model.

The above incorporates all VTY’s aims such as 4yr land bank, 12% margins, and % split between owned and partner funded land. As can be seen, ROCE comes out to 38% under this model. On paper, at least, their proposed business structure, inventory and margins make 40% ROCE targets seem plausible.

4. Revenue

One of the main risks of the partnerships model i.m.o is that the UK government essentially become their customer. Government needs to set and allocate funding for affordable housing. They are also dependent on local governments to be efficient with planning approvals.

VTY partnerships include:

Local authorities, Housing Associations and REITs

Housing associations are nonprofits that own and manage affordable housing.

Local authorities are regional government agencies that control land and public housing in a particular area.

The main department overseeing affordable housing funding is the Department for Levelling Up, Housing and Communities (DLUHC). It works through Homes England for areas outside London and the Greater London Authority (GLA) for London, ensuring funds reach local authorities and housing associations effectively.

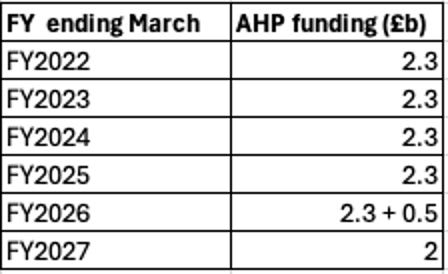

The DLUHC budget, under the Affordable Homes Program (AHP), for the 5 years 2021-2026 is a total of £11.5b (£2.3b a year).

Below is the breakdown of funding per year. FY 2026 had an additional £500m allocation approved in the November budget. FY2027 has also had a £2bn interim allocation made to provide certainty until the next 5-year budget is announced. Reportedly the next 5 year housing budget allocation is going to be larger than the previous one.

One would need to track what transpires with regard to government funded affordable housing allocations. The Labour party are at least saying that they intend to make affordable housing funding a priority.

5. Valuation

Market cap = £2b (£6 per share)

Net debt = £180m

EV = £2.2b

P/Tangible Book = 1x

LTM EV/EBIT = 6.1x

If we assume VTY unlocks £500mn via reducing the land bank and subtract that from the EV, you’ll have them trading at a LTM EV/EBIT of 4.7x. (£1.7b/£360m)

I think there is material upside to FWD EBIT, so FWD EV/EBIT is likely below 4x.

You can also look at it as a company that could realistically do >30% ROCE and trading at 1x Price/Tangible book. The 1x P/B provides decent downside protection.

Even materially lowering managements targets (40% ROCE, 12% margin) still leaves VTY very cheap. The upside here seems likely to be 200% or ~£18 per share within a 3-year timeframe.

Thank you for the detailed post. I agree that it is unlikely that the management fully hit their goals for 3 years from now, and that nonetheless if they make significant progress towards those targets there is a lot of upside to be had.

For your valuation of 200% upside in 3 years, what were your assumptions? That in 3 years the company will reach a ROCE of 30% it seems? With what margins? On what land bank volume?

Also do you have any thoughts about the long term economics of the partnership model, say in 5-10 years from today and after the full transformation has been completed, what would be the building volume (there seems to be a limit of supply), ROCE and margins?